A new chapter begins

Top considerations for defined contribution plan sponsors in 2025

Summary

According to the Alliance for Lifetime Income’s Retirement Income Institute1, the population of those aged 65 and above will hit a historical high in the US this year and for the next few years. Not surprisingly, recent landmark legislation continues to push plan sponsors to expand coverage, provide greater financial flexibility and assist in the management of retirement income, even with signs of a “Secure 3.0” legislative effort taking shape. We recognize that many defined contribution (DC) plan sponsors are overwhelmed by these legislative changes and the responsibility to set and implement an optimal path forward.

[1] Fitchner, J. (2024). The peak 65 zone is here - creating a new framework for America’s retirement security. Protectedincome.org. https://www.protectedincome.org/wp-content/uploads/2024/01/Whitepaper_Fichtner.pdf

Considerations for DC plan sponsors

Retirement income

DC plan sponsors and their providers spend a significant amount of time focused on building sizeable account balances in anticipation of retirement through plan design features, investment options, and participant engagement.

However, some retirees struggle to manage their income streams in retirement. For example, almost 70% of those who retired before they were 65 did so because of circumstances beyond their control and half of retirees indicate that their expenses in retirement are higher than anticipated.2 On the flip side, for others, fear of outliving their assets significantly limits the retirement experience.

Both scenarios indicate that retirees are under pressure to make savings last through retirement and suggest a need for help navigating both unexpected financial hurdles and sustainable spending in retirement. Understanding how to effectively draw down assets coupled with longevity risk continues to be a concern for many.

2024 brought a noteworthy step in the evolution of the retirement income landscape, with the launch of an off-the-shelf target date fund that provides participants with the option to annuitize a portion of their balance. While retirement income discussions should not be limited to investment products with annuities, we believe we are at the precipice of plan sponsors offering more robust tools, resources and investment options to support participants’ decumulation.

In 2025, DC plan sponsors should evaluate the need for retirement income and begin to establish a philosophy and roadmap for how to address decumulation informed by participant demographics. An effective retirement income offering should include varying levels of support to provide a meaningful benefit to participants.

[2] Employee Benefit Research Institute 2024 Retirement Confidence Survey

Simplification v. customization

As recordkeepers pursue efficiency in response to continued price pressures, there is an ever-increasing desire to streamline systems and processes.

A consequence is the reduced willingness and ability to provide customized plan administration. Sponsors seeking to differentiate through customized plan designs or needing greater support to compensate for challenging payroll or HRIS systems are now grappling with more rigid systems and processes that can lead to frustrations or unmet expectations for participant service.

Whether limiting sponsors’ choices in implementing Secure 2.0 optional provisions—like hardship self-certifications or small-balance distribution thresholds—or imposing additional fees for employer contribution calculations, recordkeepers are forcing sponsors to make decisions that are not necessarily aligned with their strategic objectives in order to manage costs or avoid increasing their own administrative burden.

In some situations, the drive towards simplification is impacting the participant more than the sponsor when limitations are imposed on how and when plan resources and investments can be accessed. At the end of the day, are simplification and standardization benefiting or disadvantaging the sponsor or the participant?

Less attractive economics for recordkeepers has also led to attempts to bridge revenue gaps through expanded retirement and financial wellbeing services. Proprietary managed accounts, one-on-one counseling, and rollover services can all be streams of additional revenue generation. While participants can certainly benefit from these offerings, we caution sponsors to be mindful of whether these solutions are appropriate for the participants utilizing them and to ensure there is transparency in the underlying economics.

As you plan for 2025, consider reviewing your plan from the perspective of both the participant and plan sponsor.

- Participant lens: Identify the information and functionality that participants undergoing various life events are seeking and determine whether your plan is structured to maximize the participant experience.

- Plan sponsor lens: Identify the elements of ongoing processing that have required corrections in the past or involve manual processes, then determine whether these risks can be mitigated or supported by additional value-added services.

Outsourcing

We have seen Pooled Employer Plans (PEPs) gain traction as sponsors continue to consider outsourcing the investment management and administration of DC plans.

PEP adoption has been somewhat concentrated among plans under $500 million in assets to date or for larger plan sponsors who are experiencing corporate actions, such as spin-outs and divestitures. Looking at global DC pooled plan trends, we anticipate that larger plans may also find PEPs of interest in the future.

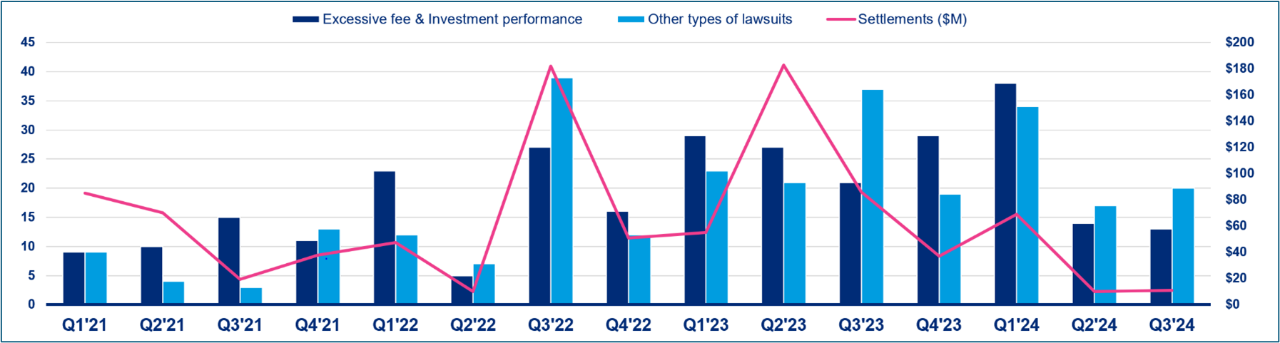

One commonly cited driver of PEP adoption, and outsourcing in general, is the continued barrage of litigation that DC plans face. While largely concentrated around fees and investment performance, 2024 saw litigation expanding into areas of administration as well.

Figure 1: Litigation trends Q1 2021 through Q3 2024

Some plan sponsors are choosing to share the risk with a qualified PEP sponsor or OCIO (outsourced chief investment officer) who is willing to act in an ERISA 3(38) capacity and/or an ERISA 3(16) capacity. Other sponsors wish to take advantage of the scale of these outsourced providers to reduce investment and administrative costs in the hopes of skirting the radar of plaintiff firms searching for fee-related lawsuits. For companies seeking to mitigate operational risk without delegating investment decision-making, the ability to offload daily oversight and management of plan investments and administration is an attractive pressure release.

As companies continue to work through the big administrative hurdles of complying with Secure 2.0 mandatory provisions, we anticipate that outsourcing may be an attractive option to help offset the additional burden that implementing changes can pose for already resource-constrained staff.

As you approach planning for 2025, consider whether some degree of outsourcing—temporary or ongoing—could bring more consistency to oversight and plan operations, perhaps while providing cost or performance improvement to participants.

Conclusion

We believe that successful retirements require building adequate financial resources and decumulation strategies. The Mercer CFA Institute 2024 Global Pension Index report continues to rank the US below other developed nations in terms of retirement adequacy, highlighting the opportunity for DC plan sponsors to continue to enhance broad retirement offerings.

The sharp increase in the number of individuals reaching retirement age in 2025 necessitates a proactive approach from plan sponsors to ensure that their offerings effectively support participants in achieving financial security throughout their retirement years.

Outsourcing presents a viable strategy for those plan sponsors seeking to professionalize investment decision-making, alleviate administrative burdens and enhance operational efficiency, allowing them to focus on strategic decision-making. There is a significant strategic opportunity for sponsors to address the decumulation phase, equipping participants with the tools and resources necessary to manage their income streams effectively and navigate the complexities of retirement spending.

Furthermore, the tension between simplification and customization underscores the importance of aligning plan design with the unique needs of both participants and sponsors. As recordkeepers streamline their processes, it is essential that sponsors advocate for flexibility that accommodates diverse participant circumstances while ensuring transparency in the services offered.

Plan sponsors have taken many positive steps over the last several years to improve retirement outcomes for participants. We see more positive changes ahead as the industry continues to develop new and enhanced solutions.